IB Docs (2) Team

IB Docs (2) Team

Perfect competition (HL only)

Introduction

Introduction

This is the beginning of the section on perfect competition. There are a number of paper one questions on this topic, some of which are included on this site. This lesson looks at the conditions of perfect competition. A fun exercise is to ask your classes to investigate industries from the real world which might be very close to perfect competition in nature. This page contains one example of a market that I believe is close, containing many of the characteristics of perfect competition.

Enquiry question

What is perfect competition? Does this market structure exist in the real world or is it purely a theoretical concept.

Teacher notes

Teacher notes

Lesson time: 75 minutes

Lesson objectives:

Describe, using examples, the assumed characteristics of perfect competition.

Explain, using a diagram, the shape of the perfectly competitive firm’s average revenue and marginal revenue curves, indicating that the assumptions of perfect competition imply that each firm is a price taker.

Explain, using a diagram, that the perfectly competitive firm’s average revenue and marginal revenue curves are derived from market equilibrium for the industry.

Teacher notes:

1. Beginning activity - begin with the opening activity and allow 10 minutes for your classes to complete the questions and discuss the video. (15 minutes)

2. Processes - technical Vocabulary - the students can learn the key concepts through the notes, which should take ten minutes to go through and discuss. (10 minutes)

3. Practise activities included on the handout should take around 35 minutes.

4. Reflection exercise - considers whether perfect competition is likely to offer low prices to consumers or not, based on what they have learnt so far. (5 minutes)

5. Link to the assessment - project the paper one style question onto the whiteboard and then allow 10 minutes for your class to discuss the essay question or even set the essay as a homework or class room exercise. (10 minutes)

Conditions of perfect competition

Very large numbers of sellers and buyers, each too small to influence the market supply/demand and hence market price. In other words, the businesses in perfect competition are price takers and not price makers.

Very large numbers of sellers and buyers, each too small to influence the market supply/demand and hence market price. In other words, the businesses in perfect competition are price takers and not price makers.

All firms sell the same homogenous (identical) product, making them indistinguishable for consumers and hence no brand loyalty. There are no branded products in perfect competition.

Perfect knowledge for both buyers and sellers. Each producer is fully aware of the costs and prices set by their competitors. Consumers are also fully aware of prices in the market and the quality and availability of those products.

Freedom of entry and exit into and out of the market. This means that firms can easily shut down should profits fall below the normal profit level and equally easily set up when abnormal profits make the market attractive.

The class exercises are available as a class handout in PDF form at: ![]() Perfect competition

Perfect competition

Beginning activity

Watch the following short video and then answer the following two questions:

(a) According to the video what are some of the assumptions of a perfectly competitive market?

(b) Which two sectors within South Africa come under criticism in the video for not operating in a competitive market?

(a) The video highlights the following conditions:

In a perfectly competitive market all market participants must be price takers, not price makers.

Many buyers and sellers in the market.

Highly competitive market, with no agreements or collusion between competing businesses in the market.

Homogenous products, with no brand loyalty.

Perfect knowledge e.g. buyers must know the price being charged by each company. This means that for instance, in a perfectly competitive market customers will not buy from companies that charge over the market price.

The market must be unregulated e.g. there must be no labour laws preventing firms from hiring and firing workers as they see fit and there must also be freedom of entry and exit into and out of the market.

(b) The video focused on the bread market and pharmaceuticals which colluded to prevent competition and drive up prices

Activity 2

The video focus on the agricultural sector in Poland, a market that some economists believe shares many of the characteristics of perfect competition. Watch the short video and then decide for your self, before deciding what makes perfect competition different to the other market structures featured in the video:

(a) Which of the conditions of perfect competition does the Polish farming sector satisfy?

A large number of buyers / sellers?

Homogenous products, hence ho brand loyalty, for example the video states that it would be impossible for one farmer to claim that their carrots were different to another farmers

All the farmers are price takers, dependent on the industry demand and supply.

(b) What differentiates the agricultural market in Poland from the retail market featured in the video?

There are many similarities but the difference is that the retail market has a level of product differentiation which makes it an example of monopolistic competition.

(c) How could the Polish farmers differentiate their products to raise prices?

Some of the avenues available to the farmers could be to differentiate their products by obtaining, for example, a certificate of authenticity to prove that the food produced met a higher degree of safety standards, or were organically produced. In some parts of the world farmers can differentiate their products by obtaining a 'fair trade' certificate, allowing them to gain higher prices for their produce.

(d) What market structures were the car industry and the water company featured in the video?

Oligopoly and monopoly.

Activity 3: Short answer questions

Start by watching the following short video which illustrates how to draw the market for a firm in perfect competition. Then complete the short questions which follow:

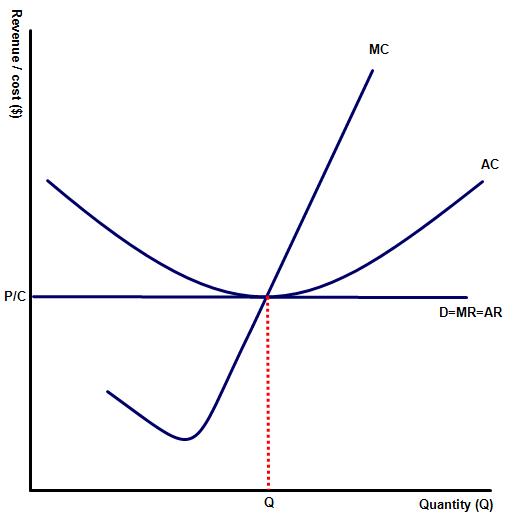

(a) What is the relationship between P and MR?

They are the same (P=MR) because TR = P*Q and since TR increases by a constant amount we know that P=MR; MR=P and since P is set by the market firms all receive it when they sell a good.

(b) Are the firms in perfect competition producing at the profit maximising level of output?

Yes, as the diagram above illustrates the firm is producing at where MC=MR.

(c) Why would demand be perfectly elastic for an individual firm in a perfectly competitive market?

The firm cannot raise or lower the price since it is a price-taker (as is the consumer). We also know then that P=MR=MR/Q (average revenue)

(d) Why is the PED elasticity for individual firms in perfect competition equal to Ѡ?

The demand curve is perfectly elastic for individual firms because they are price takers? If the firm raises price above the equilibrium level then demand will fall to 0. Similarly there is no incentive for firms to reduce their prices below the equilibrium price because they can sell all of the product they need at the original price.

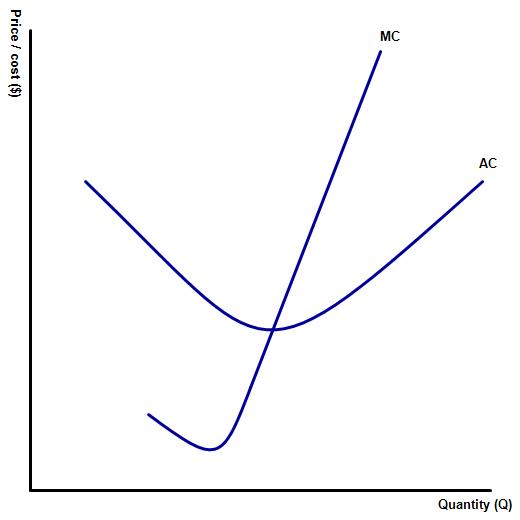

(e) Complete the diagram by drawing the AR and MR curve and mark the equilibrium level of output and price.

(e) Complete the diagram by drawing the AR and MR curve and mark the equilibrium level of output and price.

Activity 4

Based on what you have learnt about perfect competition so far, do you believe that this market structure is likely to offer low prices for the consumer, compared to less competitive structures?

This all depends on the type of product available. Perfectly competitive markets can offer low prices but they are not suitable for some types of industries e.g. the telecommunications market, car and water production e.t.c. would be wholly unsuited to a perfectly competitive structure. The homogenous products present in this market structure also limits product choice.

Activity 5: Link to the assessment (Paper one, part A type)

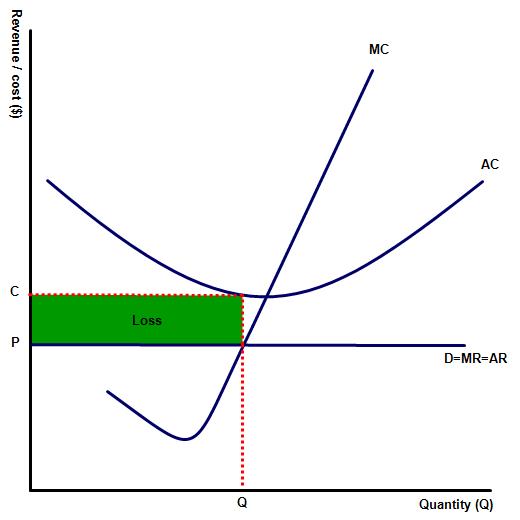

1. Illustrate with an appropriate diagram why a perfectly competitive firm can still make a loss in the short term whilst producing at the maximum profit level of output. [10 marks]

Command term: Explain

Command term: Explain

Key terms to define: perfectly competitive market, short term, marginal cost, marginal revenue.

Responses should also include a diagram showing a perfectly elastic diagram, showing short-run losses at the level of output where MC equals MR - output Q.

An explanation that the profit maximising level of output for all businesses, including perfect competition, is at the point where marginal cost equals marginal revenue. However, producing where MC = MR guarantees only that the firm will minimise losses, not necessarily make abnormal profit or even normal profit levels.

Examples of circumstances that may cause short term losses in the business e.g. a rise in production costs or a fall in demand levels.

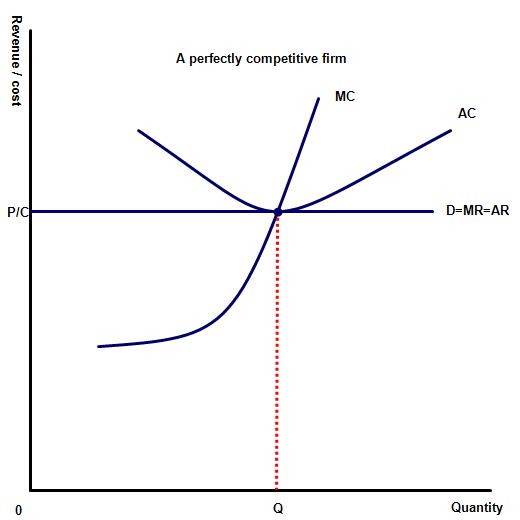

2. Explain why in perfect competition the marginal revenue curve is equal to the average revenue curve but not in other market structures? [10 marks]

Command term: Explain

Command term: Explain

Key terms to define: perfectly competitive market, MR, AR

Responses should also include a diagram showing a perfectly elastic demand curve, showing MR = AR.

An explanation that in other types of market structure, when the AR and MR are straight lines, sloping downwards, the marginal revenue falls at twice the rate of the average revenue. In other words, the marginal revenue will cut any line perpendicular to the y – axis at halfway to the average revenue curve. This can be proved mathematically and should be illustrated with an appropriate diagram, such as the one to the left, showing a monopoly firm.

to the y – axis at halfway to the average revenue curve. This can be proved mathematically and should be illustrated with an appropriate diagram, such as the one to the left, showing a monopoly firm.

By contrast in perfect competition the demand curve is perfectly elastic there is no slope on the AR / demand curve and hence no slope to the MR curve. This can be explained by the fact that in perfect competition it is assumed that individual firms can sell all of their produce at the same price, as they are too small to influence market supply and therefore price.

Twitter

Twitter

Facebook

Facebook

LinkedIn

LinkedIn